Meet Satoshi Nakamoto's 12 Apostles

Defining Satoshi’s twelve apostles isn’t as easy as it seems. For one thing, some of the contenders are among his predecessors. On the other hand, there are hundreds of cryptocurrency pioneers who are doing amazing things in the blockchain and crypto space. So how do you define what an apostle is?

The word comes from Classical Greek and literally means “one who is sent” or “one who is commissioned with a message.” In a word, an apostle is an emissary, or envoy. A representative.

More than one major religion uses the word to signify important people in the history of that religion. In Christianity, the 12 apostles were commissioned by Christ himself to carry out his message after he was crucified and buried. In Islam, various prophets throughout history are referred to as messengers, or “apostles.” In one sense of the word, it also signifies “laying the groundwork.” That is, an apostle could also be a foundation layer.

If we get too literal with the use of the word, it might not mean much at all in the case of cryptocurrency. As far I know, there is only one possible individual in the following list who might have been appointed or specially commissioned to carry on Satoshi’s work. There is one other individual who was the first recipient of a bitcoin transaction. Others on the list simply took it upon themselves to spread the message about the new technology channeled through Satoshi’s brain. In any case, each of the following individuals are significant in one way or another to the development and growth of the early days of cryptocurrency.

What I tried to do is narrow the list down to significant individuals who had a direct relationship with Satoshi Nakamoto in one way or another and made at least one significant contribution to the growth and development of bitcoin before Nakamoto’s disappearance in 2011 or made big multiple significant contributions or one huge contribution to the development of the cryptocurrency ecosystem between 2011 and 2014.

Hal Finney

Hal Finney made two significant contributions to the early development of bitcoin. The first is that he was the first recipient of bitcoin, which Satoshi Nakamoto sent to him to test his new technology. Finney received 10 bitcoin.

The second contribution Finney made is he helped Satoshi Nakamoto work out some bugs in bitcoin’s programming. This happened just a few days after receiving the 10 bitcoin from the technology’s inventor.

Not long after that final event, Finney announced that he’d been diagnosed with Lou Gehrig’s disease. He died from complications five years later. Who knows what greatness he might have achieved if he'd have lived longer?

Adam Back

Adam Back is significant to bitcoin’s development in a couple of ways. First, as inventor of the proof-of-work system on which bitcoin is based, Back is one of the few pioneers in cryptocurrency to be cited in Nakamoto’s bitcoin whitepaper. Here’s what he had to say about Back on page 3 of the 9-page paper:

To implement a distributed timestamp server on a peer-to-peer basis, we will need to use a proof-of-work system similar to Adam Back's Hashcash [6], rather than newspaper or Usenet posts. The proof-of-work involves scanning for a value that when hashed, such as with SHA-256, the hash begins with a number of zero bits. The average work required is exponential in the number of zero bits required and can be verified by executing a single hash.

When prognosticators try to solve the mystery of Satoshi Nakamoto’s identity, Back is one of the people mentioned as most likely to be the inventor of bitcoin, though he has denied that he is the one. Nevertheless, Nakamoto contacted Back before publishing the whitepaper to let him know that he was going to be mentioned. In fact, Back is only one of two people to receive an email from bitcoin’s inventor early on.

Back has supported bitcoin development from the beginning. In 2014, believing that development wasn’t happening fast enough, he created Blockstream, a company focused on “building the blockchain technology of the future.”

Gavin Andresen

If anyone stands out as an appointed heir to Satoshi Nakamoto, it’s Gavin Andresen. In 2010, he became one of the principle developers of bitcoin. He also is known for starting the first bitcoin faucet, which is a reward system designed to distribute free bitcoin to its users. In the same year, he created an escrow serviced named ClearCoin, which shut down in 2011.

Another event that happened in 2011 is the disappearance of Nakamoto. His final email was sent to Andresen. It read:

I wish you wouldn’t keep talking about me as a mysterious shadowy figure, the press just turns that into a pirate currency angle. Maybe instead make it about the open source project and give more credit to your dev contributors; it helps motivate them.

When Andresen replied that he’d been invited to speak at a conference, Nakamoto never responded.

In 2012, Andresen started the Bitcoin Foundation, a nonprofit whose mission was to promote bitcoin development. After a series of controversies, Andresen stepped down from his position as lead developer of Bitcoin Core. That was 2014. Three years later, he expressed support for competing cryptocurrency Bitcoin Cash.

Laszlo Hanvecz

Two years after Nakamoto published his famed whitepaper, Laszlo Hanvecz made the first commercial transaction with bitcoin. He bought two pizzas for 10,000 BTC.

Jed McCaleb

Another event that took place in 2010 is the founding of the Mt. Gox bitcoin exchange. It was not the first bitcoin exchange. That distinction goes to Bitcoin Market. Founded in January 2010, it went live in March. Mt. Gox launched three months later.

Jed McCaleb launched the exchange that controlled 70 percent of the worldwide bitcoin trading volume by 2013.

McCaleb was not responsible for all of that growth. He had sold Mt. Gox in 2011. Two months after its purchase, the site was hacked resulting in thousands of dollars in losses to traders. That was the beginning of the exchange’s troubles. The site went on to face legal issues, lawsuits, a fraud investigation, and ultimately, bankruptcy. The site was shut down in 2014.

Meanwhile, McCaleb went on to co-found competing blockchain company Ripple, whose cryptocurrency XRP has enjoyed the third highest market capitalization for most of its life. In 2013, he left that project and co-founded another cryptocurrency called Stellar.

McCaleb’s technical programming skills are what made him one of the most successful and richest cryptocurrency entrepreneurs on the planet. And his connection to Satoshi Nakamoto is almost direct. In 2018, the New York Times named him one of the top ten people leading the blockchain revolution.

Charlie Lee

Charlie Lee’s connection to cryptocurrency is so formidable his Twitter handle is @Satoshilite. In 2011, he was a computer scientist employed by Google and began to take an interest in bitcoin. He immediately began work on a new cryptocurrency called Litecoin and released it just a few months later. By 2017, it was the fourth largest cryptocurrency by market cap. That year, Lee also sold all of his Litecoin citing a perceived conflict of interest.

Lee left Google in 2013 and went to work for Coinbase, the largest American cryptocurrency exchange at the time. Since 2018, he’s been working on Litecoin full time.

Vitalik Buterin

If there is anyone in the crypto world with the power and authority of Apostle Paul, considered the “Apostle to the Gentiles” by Christians and author of most of the New Testament, it’s Vitalik Buterin.

Buterin co-founded Bitcoin Magazine in 2011 and launched Ethereum, the second largest cryptocurrency by market cap, in 2013. These two developments alone are enough to solidify his place in history for two centuries.

Born in Russia to a computer scientist, Buterin and his family moved to Canada when Buterin was a child. He was educated in Toronto. He learned about bitcoin from his father and took an interest immediately. Then he dropped out of college to start Ethereum with a $100,000 grant from Thiel Fellowship, founded by tech investor Peter Thiel. His brilliance is unmatched in the crypto world.

Roger Ver

Few people in the crypto world have done more to promote bitcoin than Roger Ver. That’s why he’s earned the nickname Bitcoin Jesus.

Ver has an interesting history. In 2002, he pleaded guilty to selling illegal explosives on eBay. He made his first bitcoin investment in 2011. After supporting Bitinstant, he began to back other cryptocurrency projects including Ripple, Blockchain.info, Bitpay, and Kraken. He also owned a company in 2011 called Memorydealers that became the first company to accept bitcoin payments. Ver went on to organize Meetups around bitcoin and co-founded the Bitcoin Foundation.

One of the most colorful characters in the bitcoin drama, Ver renounced his U.S. citizenship and moved to Saint Kitts and Nevis in 2014. In 2017, he supported a bitcoin fork and started evangelizing Bitcoin Cash. He also served as CEO of Bitcoin.com until 2019.

Ross Ulbricht

Other than Nakamoto himself, few people connected to bitcoin are as controversial as Ross Ulbricht and very few draw as much ire. Best known as the creator of the darknet Silk Road, Ulbricht may be the man most responsible for associating bitcoin with criminal activity in the minds of some people.

Ulbricht was born in 1984 in Austin, Texas. A boy scout, he attained to the rank of Eagle Scout and attended the University of Texas at Dallas before seeking a master’s degree from Pennsylvania State University. That was when he took an interest in libertarian economic theories. After graduation, he returned to Austin and started a video game company.

The year 2010 is when Ulbricht began working on Silk Road. In a private journal, he wrote, “I am creating a year of prosperity and power beyond what I have ever experienced before. Silk Road is going to become a phenomenon and at least one person will tell me about it, unknowing that I was its creator.” Everything fell apart for Ulbricht in 2013 when he was arrested for running an illegal drug operation.

Ulbricht wasn’t actually dealing drugs, but he profited from drug trafficking. Silk Road was an underground internet community that utilized Tor technology in connection with bitcoin that allowed drug dealers, hitmen, child pornographers, and other seedy criminals to conduct their illegal business transactions with anonymity. It was that way by design, but it was naivete and Ulbricht’s diehard commitment to libertarianism that did him in. When he was offered a plea deal, he rejected it. In sentencing, he received two life sentences plus forty years without parole.

In December 2020, Ulbricht’s name came up again when The Daily Beast reported that President Donald Trump was considering a pardon for him.

Charlie Shrem

If it seems like 2011 is a magical year for bitcoin, that’s because it is. It’s the year Satoshi Nakamoto disappeared without a trace leaving Gavin Andresen in charge of development. It’s also the year Jed McCaleb sold Mt. Gox. It’s the year Charlie Lee and Roger Ver took an interest in bitcoin. It’s also the year Ross Ulbricht launched Silk Road and when Vitalik Buterin co-founded Bitcoin Magazine and launched Ethereum. That same year, Charlie Shrem was a senior in college and started his bitcoin journey.

After facing some challenges with buying and selling bitcoin through existing services, Shrem found a partner and launched BitInstant.

To launch the bitcoin exchange service, he borrowed $10,000 from his parents. The company grew quickly and attracted investments from others, including the aforementioned Ver and the Winklevoss twins. By 2013, BitInstant was processing 30 percent of all bitcoin transactions. The future looked bright. Then Shrem was arrested.

When the Bitcoin Foundation was founded in 2012, Shrem was one of its five co-founders. He resigned as vice chair after his arrest.

Even as he was on trial, Shrem was out promoting bitcoin. He was convicted in 2014 on charges of indirectly facilitating $1 million in digital currency transfers through Silk Road. Shrem served his prison time from March 2015 to June 2016. After his release from prison, he’s been very active in promoting bitcoin by appearing in documentaries, founding crypto companies, acting as executives in others, and became an active supporter of upstart cryptocurrency Dash in 2017. Two years later, he launched a bitcoin podcast called Untold Stories. He was also the target of a lawsuit by the Winklevoss twins, no strangers to suing technology mavens, but that was later dropped.

Shrem is evidence that sometimes what a revolution needs most is a martyr.

Andreas Antonopoulos

Born in London, Andreas Antonopoulos took an interest in bitcoin in 2012. In wild abandon, he quit a freelance consultancy he had as a computer scientist and started a public speaking career to promote bitcoin. He has written several popular books on cryptocurrencies since then.

In 2014, Antonopoulos led a fundraiser for Dorian Nakamoto, who had been incorrectly identified as Satoshi Nakamoto by journalists whose reporting tactics became controversial. The event disrupted Dorian Nakamoto’s life, but the bitcoin community raised $23,000 in bitcoin for him.

Antonopoulos has also appeared before governments to answer questions about bitcoin for regulatory consideration.

Dan Larimer

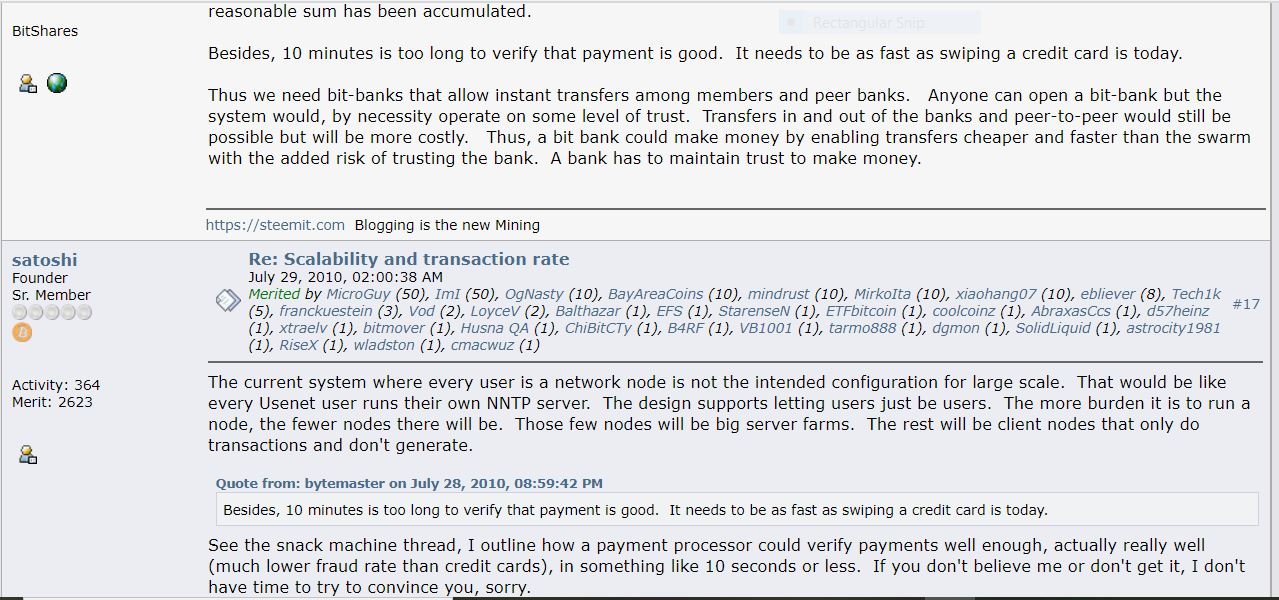

Daniel Larimer is the late bloomer of the bunch. In 2020, he started a blog titled More Equal Animals, a reference to George Orwell’s famous literary classic Animal Farm, in which he consolidated all of his blogs from the past six years. On his About page, he tells how he was working on the creation of a digital currency in 2009 when he stumbled upon bitcoin. He even had an encounter in the popular bitcoin forum with Satoshi Nakamoto where the latter famously responded to Larimer, posting as Bytemaster, with a terse, “If you don’t believe me or don’t get it, I don’t have time to try to convince you, sorry.”

While Larimer discovered bitcoin in 2009, he didn’t become active in blockchain development until much later.

In 2014, Larimer co-founded decentralized cryptocurrency exchange Bitshares with Charles Hoskinson, who went on to create the cryptocurrency Cardano. In doing so, Larimer invented the delegated proof-of-stake consensus (DPOS) mechanism, which works considerably different that bitcion’s consensus mechanism, called proof of work. Larimer went on to co-found Steem and Block One, both blockchain companies, and launched Steemit, the first blockchain-based social media platform. He also co-founded blockchain-as-a-service company eosio and Voice, his latest project, which is also a social media platform based on blockchain technology. Additionally, Larimer was the first person in blockchain circles to talk about decentralized autonomous organizations (DAOs).

Unlike other crypto pioneers, Larimer has managed to stay out of legal trouble and does not have a string of failed projects behind him. He has a strong development background and bases much of his development and blockchain philosophy on libertarian principles, which he discovered in 2005.

Larimer is different than many of the other people on this list in that he does not seek out the limelight. He is not often front and center on the projects he takes on, preferring instead to sit in the background. But his genius is evident in every project he pours himself into. He is one of the few disciples of Satoshi Nakamoto to have captured the spirit of bitcoin as well as the vision of its founder and maintained a philosophical purity that is compatible with it.

Other Contenders

There are many brilliant minds working blockchain development. The above list represents, to me, a short list of early pioneers who captured the spirit and essence of bitcoin and became its chief evangelists from 2011 to 2014. The following list of people are also significant early adopters or players in the bitcoin space.

Brian Armstrong founded Coinbase, the largest cryptocurrency exchange in the U.S., in 2012. By 2014, Coinbase had 1 million users.

Cameron and Tyler Winklevoss invested in bitcoin early. In 2013, they claimed to own almost 1 percent of all bitcoin at the time. The also invested in early bitcoin startups like BitInstant and went on to found a cryptocurrency exchanged called Gemini.

Mark “Slush” Palatinus created the first bitcoin mining pool, called Slushpool, in 2010.

Charles Hoskinson co-founded Ethereum and Bitshares. He was also the chief developer of Cardano.